AI is dominating the 2026 unicorn pipeline, as record-breaking investment accelerates the creation of billion-dollar startups across sectors

A surge in funding is not only creating more unicorns—it’s reshaping which technologies define the next wave of global innovation.

AI Leads a Record-Breaking Year

Venture capital is on track for a record year in 2026, with artificial intelligence startups already attracting over $220 billion in funding globally by March—nearly matching the total raised across all sectors in 2025.

According to new analysis from BestBrokers, this surge is rapidly transforming the unicorn landscape. So far this year, 47 startups have crossed the $1 billion valuation threshold, officially joining the unicorn club.

AI companies account for the largest share of these new entrants, representing roughly a quarter of all new unicorns—by far the dominant sector.

A New Unicorn Landscape

The data highlights how concentrated this growth has become.

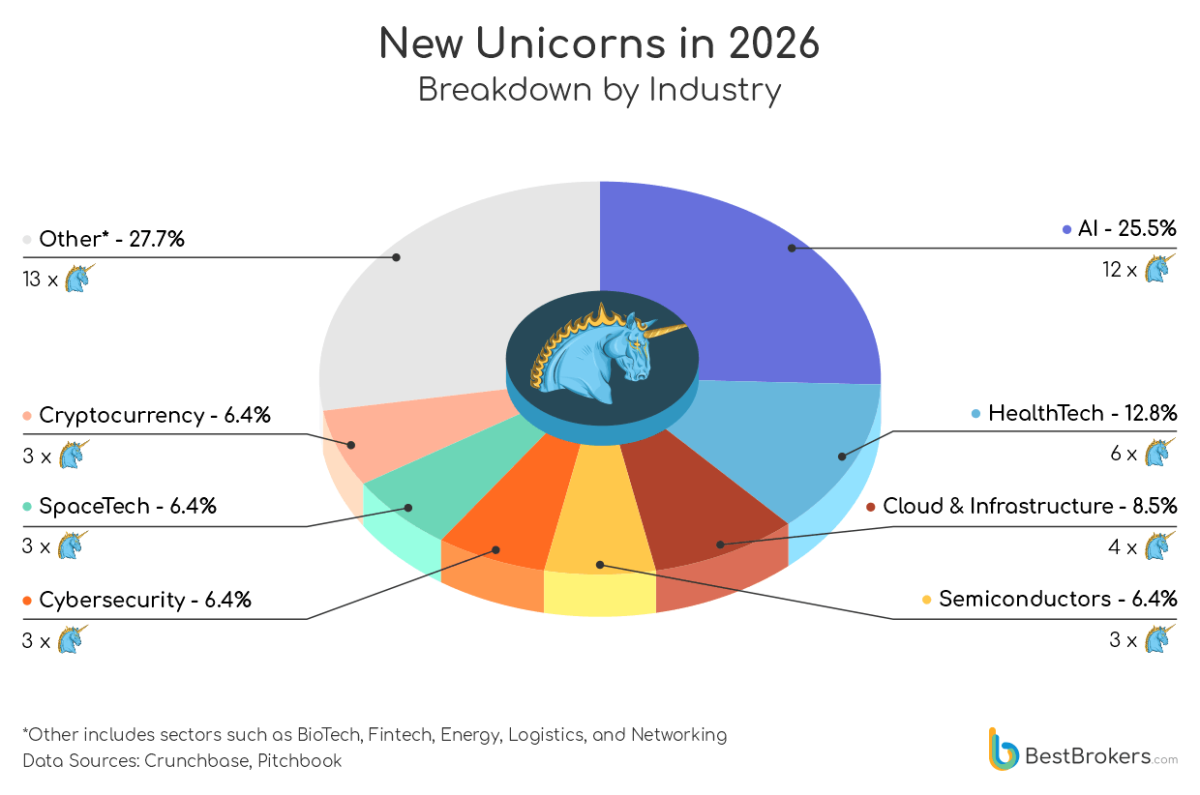

Breakdown of new unicorns by sector:

-

AI — 25.5% (12 companies)

-

HealthTech — 12.8% (6 companies)

-

Cloud & Infrastructure — 8.5% (4 companies)

-

Semiconductors — 6.4% (3 companies)

-

Cybersecurity — 6.4% (3 companies)

-

SpaceTech — 6.4% (3 companies)

-

Cryptocurrency — 6.4% (3 companies)

-

Other sectors — 27.7% (13 companies)

This distribution shows that while AI dominates, there is also strong investor appetite for the infrastructure and adjacent technologies required to support it.

The Most Valuable New Entrants

Among the newly minted unicorns, AI companies are not just the most numerous—they are also the most valuable.

Leading the group is California-based humans&, which reached a valuation of $4.5 billion, backed by major investors including NVIDIA, GV, Emerson Collective, and SV Angel.

Other standout companies include:

-

Ricursive Intelligence (AI) — $4.0B

-

Rain (Crypto & Blockchain) — $1.9B

-

Bedrock Robotics (Robotics) — $1.8B

-

Roark Aerospace (DefenseTech) — $1.8B

-

Pomelo Care (HealthTech) — $1.7B

This reinforces a broader trend: AI is commanding both volume and valuation leadership.

The Geography of Innovation

The geographic concentration of unicorn creation is equally striking.

-

United States — 36 companies

-

China — 3 companies

-

United Kingdom — 2 companies

-

Others — spread across Bahrain, Israel, Sweden, Australia, Belgium, and Singapore

The dominance of the U.S. reflects its continued strength in venture capital, AI research, and startup ecosystems.

Building the AI Economy

One of the most important insights from the data is that investment is not limited to AI applications alone.

As BestBrokers analyst Alan Goldberg notes:

“The current boom is as much about building the foundations of the AI economy as it is about the models themselves.”

This is reflected in strong funding for:

-

Cloud infrastructure

-

Semiconductors

-

Cybersecurity

-

Robotics

Together, these sectors form the backbone of scalable AI systems.

What This Means for the Market

The 2026 unicorn wave suggests a structural shift in how capital is being deployed.

Key takeaways:

-

AI is now the primary driver of new unicorn creation

-

Investors are backing full-stack ecosystems, not just applications

-

Infrastructure is emerging as a parallel investment priority

-

Geographic concentration remains high, particularly in the U.S.

This indicates that the current cycle is not just hype—it is a coordinated build-out of long-term technological capacity.

Conclusion

The latest unicorn data paints a clear picture: AI is not just leading the market—it is redefining it.

With record levels of funding and a growing ecosystem of supporting technologies, the next generation of billion-dollar companies is being built around AI at every layer.

The question now is not whether AI will dominate the next wave of innovation—but how broadly that dominance will extend across industries.